July 30, 2025

Updated: July 30, 2025

From compliance to cost savings, discover why pen testing is your best ally in securing affordable and reliable cyber insurance in 2025.

Mohammed Khalil

In today's digital world, cybersecurity isn't just about preventing data breaches; it's about business continuity and survival. The threat landscape is evolving at a breakneck pace, making robust security measures and comprehensive financial protection more critical than ever. This is precisely where penetration testing steps in as a vital tool, not only for hardening an organization's defenses but also for navigating the increasingly complex world of cyber insurance.

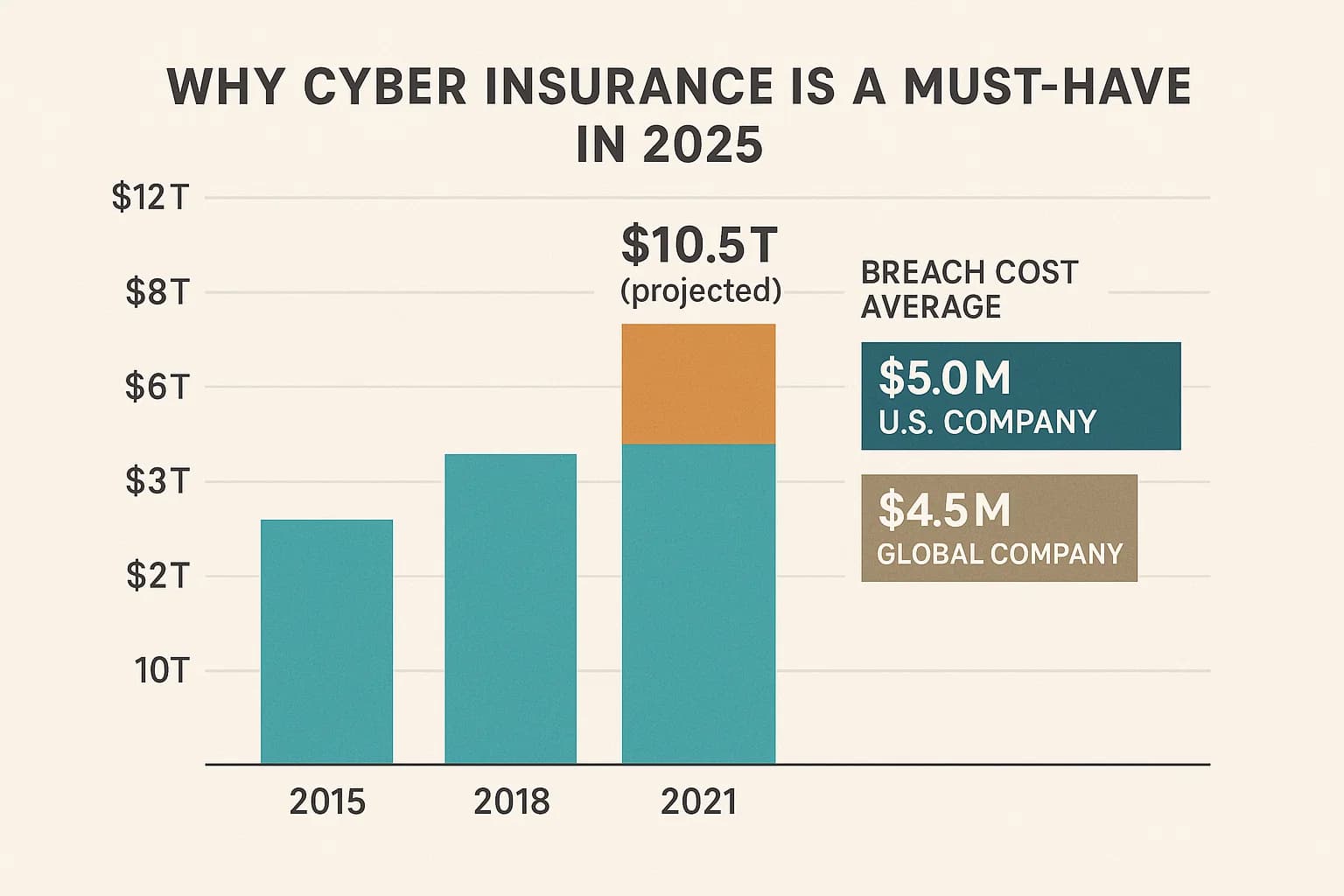

The financial toll of cybercrime is staggering and accelerating. By 2025, global cybercrime is projected to cost the world $10.5 trillion annually, surpassing the economic damage caused by all natural disasters and the global illegal drug trade combined.

In 2024 alone, the average cost of a single data breach reached a record $4.88 million, marking a 10% increase from 20232. In the United States, breach costs were even higher exceeding $9 million per incident, the highest globally.

Threats like ransomware and business email compromise (BEC) remain relentless, with estimates indicating that four companies fall victim every minute, and the average recovery cost now exceeds $4.54 million.

Meanwhile, phishing remains the top initial attack vector, playing a role in 36% of all breaches, and has become dramatically more dangerous. Since 2022, AI driven phishing attacks have increased in sophistication by over 4,000%, bypassing traditional detection tools and user awareness training.

These aren’t theoretical risks, they're existential threats. For most organizations, it’s no longer a question of if a breach will happen, but when. And with rising breach costs and legal liabilities, cyber insurance has shifted from a luxury to a business critical safeguard.

Given these alarming statistics, cyber insurance has transitioned from a luxury to a fundamental business necessity. It's a specialized product designed to shield organizations from the financial repercussions of cyber incidents. This coverage can include everything from lost income due to ransomware attacks, legal actions stemming from data breaches, costs associated with digital forensic investigations, data and system restoration, and even expenses for replacing "bricked" devices and fulfilling breach notification requirements. It's important to note that general liability policies typically exclude cyber liability, creating a critical gap in traditional business protection that only specialized cyber insurance can fill. This explicit exclusion means traditional insurance models don't adequately assess or price cyber risks, which are dynamic, complex, and can lead to unique types of damages like reputational harm and regulatory fines. This forces businesses to acknowledge cyber threats as a distinct and significant category of risk requiring specialized financial mechanisms. It also indicates that insurers, having faced significant losses, are becoming much more stringent about who they cover and under what conditions.

This brings us to the pivotal role of penetration testing. Penetration testing is considered "key to qualifying for cyber insurance" because it proactively helps organizations identify and fix vulnerabilities before malicious attacks can exploit them. Many insurers now explicitly require regular penetration tests to accurately assess an applicant's risk, determine coverage eligibility, and potentially offer lower premiums. This demonstrates to the insurance provider that an organization takes cybersecurity seriously and is actively engaged in reducing known vulnerabilities. Penetration testing acts as a crucial bridge between an organization's theoretical security posture and its real world resilience, translating abstract security measures into tangible, auditable proof that directly influences financial risk assessment by insurers. This validation isn't just about finding bugs; it's about demonstrating "due care" and a proactive risk management strategy. For insurers, it means a lower likelihood of claims and a clearer understanding of the remaining risk. For businesses, it's about transforming cybersecurity from a cost center into a tangible asset for financial protection.

To truly appreciate how penetration testing impacts cyber insurance, it's essential to understand what it entails. Think of it as hiring a team of ethical hackers to try and break into your systems, but with your full permission and a clear roadmap for fixing what they find.

The National Institute of Standards and Technology (NIST) provides a clear definition: penetration testing is "security testing in which evaluators mimic real world attacks in an attempt to identify ways to circumvent the security features of an application, system, or network". This isn't just a theoretical exercise. It often involves "issuing real attacks on real systems and data, using the same tools and techniques used by actual attackers". A critical aspect of this approach is looking for "combinations of vulnerabilities on a single system or multiple systems that can be used to gain more access than could be achieved through a single vulnerability".

The emphasis on "mimicking real world attacks" and "combinations of vulnerabilities" highlights that penetration testing goes beyond surface level checks; it uncovers complex attack chains that automated tools often miss, providing a more realistic risk assessment. Modern attackers rarely exploit a single, isolated vulnerability. Instead, they chain together seemingly minor flaws, perhaps a path traversal vulnerability combined with an open redirect, or a weak password used in conjunction with an unpatched system to achieve a high impact outcome like an account takeover or data exfiltration. This is why a manual approach, like that offered by Deepstrike, which focuses on mimicking real threat actors, is critical for truly understanding an organization's real world security posture.

It's common to confuse penetration testing with vulnerability assessments, but they serve distinct purposes.

A Vulnerability Assessment (VA) is like a broad, automated health check. It uses specialized scanning tools (such as Nessus, OpenVAS, or Nmap) to identify potential security weaknesses, answering the questions of "what" vulnerabilities exist and "where" they are located. Think of it as an X ray of your security posture: it systematically "rattles every doorknob and checks every window to see if they are unlocked," producing a list of all unsecured entry points without attempting to go inside. A VA identifies vulnerabilities but does not exploit them.

In contrast, Vulnerability Assessment is a deep, manual, and goal oriented attack simulation performed by an ethical hacker. It actively exploits identified vulnerabilities to determine "how" much damage an attacker could inflict and "so what" the real world business impact would be. This is more like an MRI: it uses the unlocked door found by the VA to enter the room, explore the building, and determine what an intruder could steal or damage, demonstrating the real world consequences of identified weaknesses.

The distinction is crucial for cyber insurance. Insurers aren't just interested in a list of potential flaws; they want to know the actual risk of a breach and its potential financial impact. A VA might report a "weak password policy," but a PT would demonstrate an actual account takeover resulting from that policy, perhaps by exploiting a deep link vulnerability or a mass assignment technique. This "proof of concept" is what truly validates an organization's security posture and helps insurers quantify risk for underwriting. It moves beyond theoretical vulnerabilities to demonstrate exploitability, which is what insurers truly care about when assessing potential claims.

Another common comparison is between penetration testing and bug bounty programs. While both aim to find vulnerabilities, their goals, scopes, and operational models differ significantly.

Bug Bounty focuses on assurance and compliance. It's a deep, point in time security assessment with a narrow, strictly defined scope, typically performed by a small, vetted team of certified professionals for a fixed fee. The deliverable is a formal, comprehensive report, making it ideal for compliance audits like pci dss penetration testing or soc 2 penetration testing, pre launch assessments, testing internal systems, and establishing a security baseline.

A Bug Bounty, on the other hand, aims for continuous discovery of a broad range of vulnerabilities in live applications. It leverages a diverse, global pool of researchers for ongoing feedback, operating as an "always on" system with a broad, evolving scope and a pay for results cost model. The output is a continuous stream of individual bug reports. Bug bounties are best for mature, live applications with continuous integration/continuous deployment (CI/CD) pipelines, and for finding novel or business logic flaws.

These two approaches are complementary. A resilient security posture often combines periodic, in depth penetration tests to build a strong foundational security baseline with an "always on" bug bounty program for continuous testing of public facing assets. However, for cyber insurance qualification, penetration testing holds a unique advantage. Insurers often look for formal, comprehensive reports from reputable firms to satisfy their due diligence requirements. While bug bounties certainly contribute to overall security, their continuous, fragmented reporting model might not directly fulfill the specific, documented audit requirements of an insurance underwriter, especially for compliance frameworks like PCI DSS, HIPAA, or SOC 2, where a formal report from a reputable firm is explicitly sought. This makes the structured deliverable of a penetration test uniquely valuable for insurance purposes.

The world of penetration testing isn't one size fits all. Organizations can conduct tests on various assets, including applications, APIs, routers, source code, and other network components. This diversity reflects the complex and expanding attack surface of modern businesses.

Specialized penetration testing services include:

The testing methodology can also vary in terms of knowledge provided to the testers:

The diverse types of penetration tests reflect the complex and expanding attack surface of modern businesses. Insurers aren't just looking for a "check the box" test; they expect a tailored approach that addresses the specific risks of an organization's unique digital footprint, from web applications to cloud environments. With the rise of cloud adoption (82% of breaches involve cloud data) and API related incidents (63% of organizations experienced an API related incident in the last year) , insurers are increasingly scrutinizing these specific attack vectors. A generic network scan won't suffice. They expect businesses to conduct tests that directly address their unique risk profile, whether it's a mobile application, complex APIs, or cloud infrastructure. This means a "one size fits all" pen test report won't impress; a targeted, relevant test is key for eligibility and favorable terms.

Understanding the scope of cyber insurance and the sheer financial impact of cybercrime helps clarify why penetration testing has become such a critical component of securing coverage.

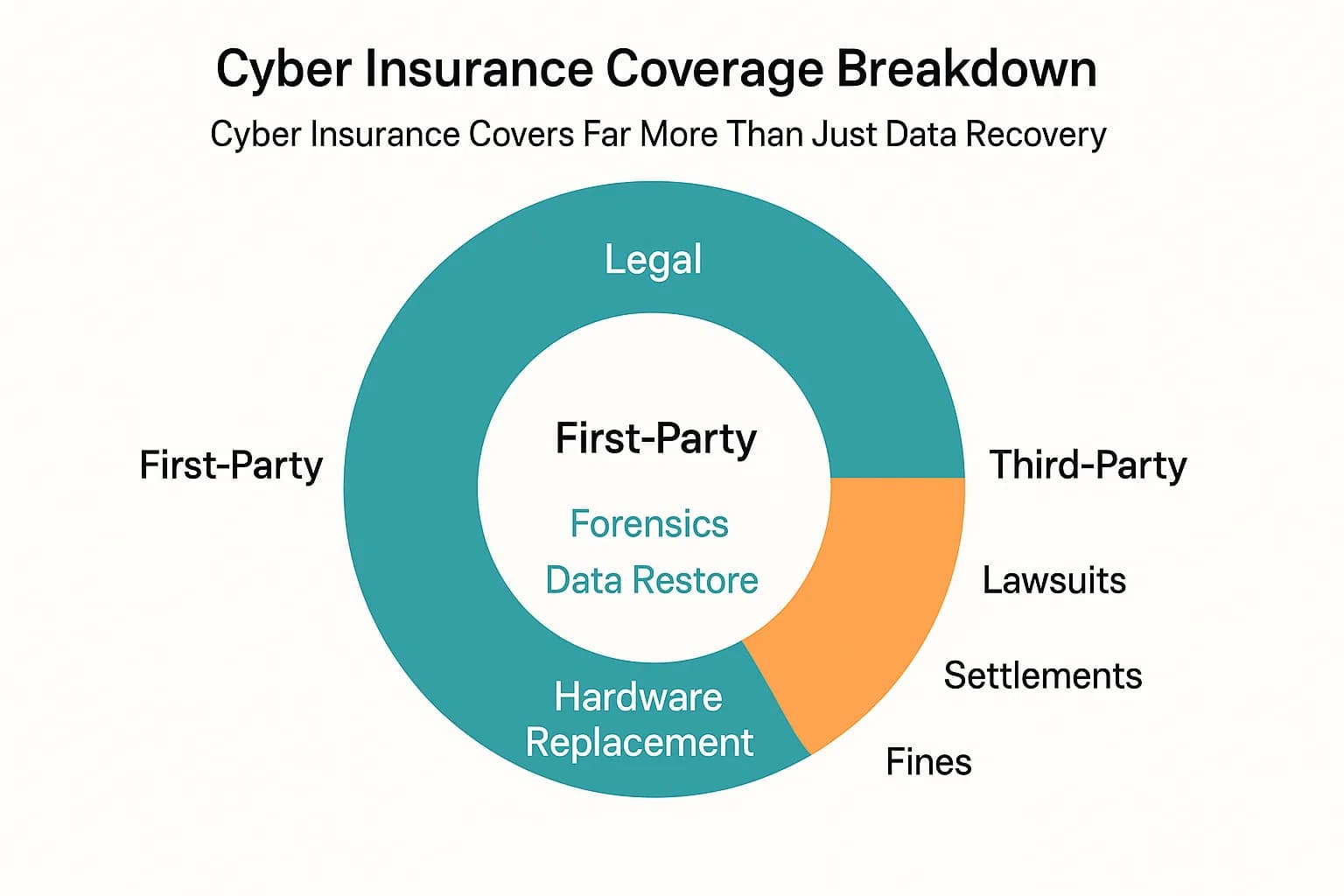

Cyber insurance is designed to cover a wide array of financial losses resulting from cyber events. These coverages typically fall into two main categories:

The comprehensive nature of cyber insurance coverage, encompassing both direct financial hits and broader legal liabilities, underscores a crucial point: cyber insurance isn't just about covering the immediate financial impact; it's about managing the complex, multi faceted fallout of a cyberattack, including legal liabilities and reputational damage. This comprehensive coverage reflects the interconnected nature of modern cyber risk. The inclusion of third party liability emphasizes that cyberattacks have ripple effects beyond the immediate victim organization. They impact customers, partners, and regulators, leading to significant legal and reputational costs that can far outweigh direct recovery expenses. Insurers are essentially underwriting not just technical failure, but also the cascading legal and trust implications. This makes proactive measures like penetration testing even more valuable, as they aim to prevent these complex, costly scenarios from materializing.

The escalating financial devastation caused by cybercrime transforms cyber insurance from a "nice to have" to a fundamental pillar of business resilience in 2025. It's not just about covering losses, but about ensuring survival, especially for small and midsize businesses (SMBs).

Consider these stark figures:

These statistics paint a picture of a threat landscape where cyberattacks are not just incidents, but potential catastrophic business events. For many organizations, particularly SMBs, the financial impact of a breach without insurance is simply unrecoverable. This makes cyber insurance a de facto operational necessity, akin to property or general liability insurance. This intense financial pressure on businesses, combined with insurers' own losses, creates a feedback loop: businesses need insurance more than ever, and insurers need proof of reduced risk more than ever. This is why penetration testing, as a verifiable measure of security posture, becomes a non-negotiable requirement, driving a shift from reactive to proactive security investments.

This is where the rubber meets the road. Penetration testing isn't just about finding bugs; it's about building a credible case for your organization's cybersecurity maturity to insurance providers.

For insurers, the core question is whether an organization has exercised "due care" in protecting its assets from cyber threats. Penetration testing is considered "key to qualifying for cyber insurance" precisely because it helps identify and fix vulnerabilities before attacks occur. Many insurers mandate regular

penetration tests to assess risk and determine coverage eligibility. The results validate the likelihood of a breach and pinpoint potential threats, unequivocally demonstrating that an organization "takes cyber security seriously".

It's a harsh reality that cyber insurance claims are frequently denied. Common reasons cited by insurers include "inadequate security measures" or "poor prevention practices". This highlights a crucial point: a self attested questionnaire response is merely a statement of intent. What insurers demand is objective, third party validation that industry recognized security controls are not only implemented but are

effective against real world attack techniques. A penetration test report provides precisely this unbiased, expert assessment, giving underwriters the confidence to offer coverage rather than deeming the applicant a high risk. This external verification is critical for insurers to trust that "due care" has been exercised, directly influencing eligibility.

Beyond mere eligibility, penetration testing directly influences the cost of cyber insurance. Many insurance companies offer lower data breach insurance premiums to organizations that conduct regular penetration tests. Insurers factor in the likelihood of a claim when setting premiums; naturally, a lower risk profile translates to a lower premium.

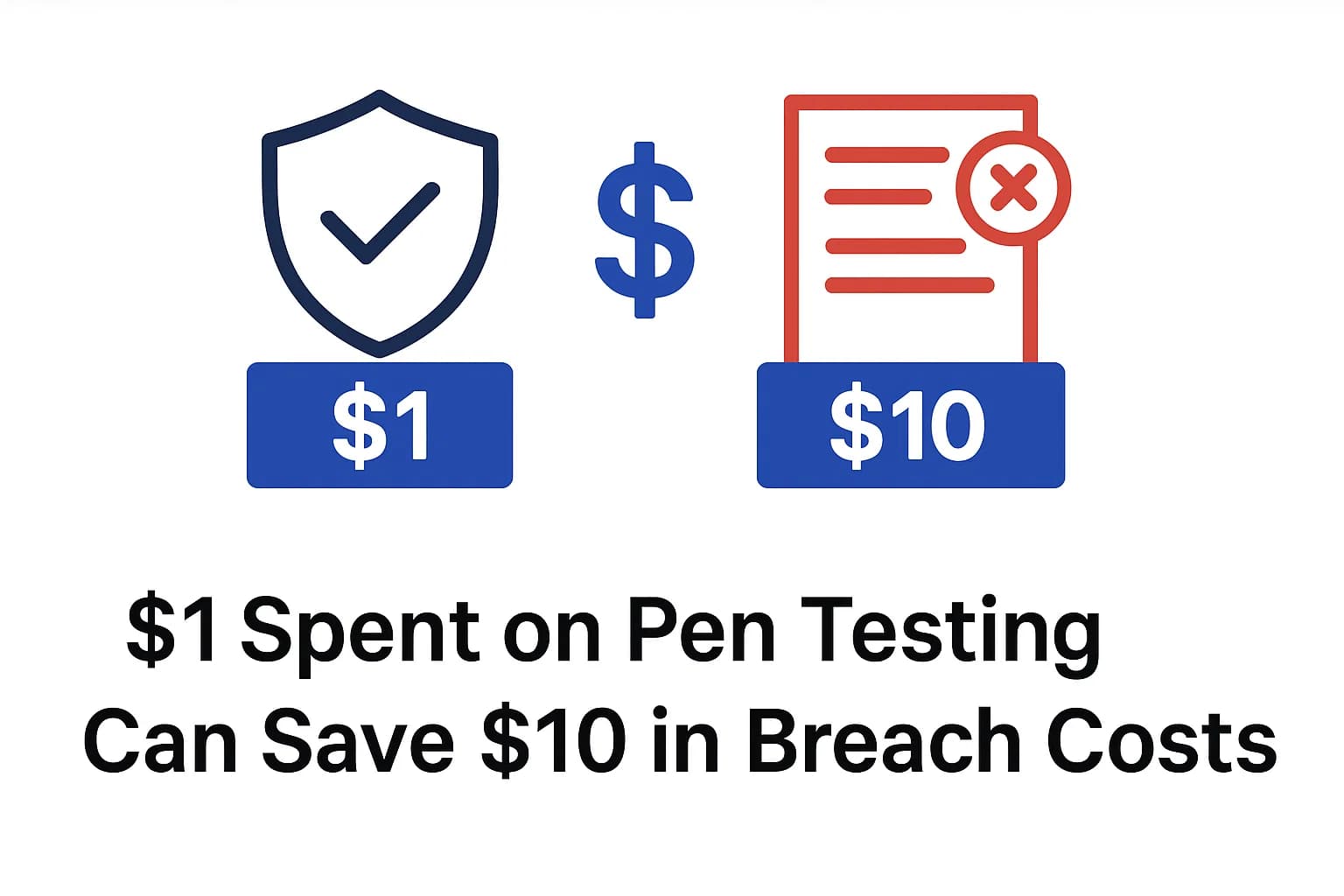

The financial benefits extend beyond just insurance savings. Studies indicate that for every $1 spent on penetration testing, organizations can save up to $10 in potential breach costs. This makes penetration testing a strategic investment with a tangible return on investment (ROI), directly impacting the bottom line through reduced insurance costs and avoided breach expenses. This financial incentive reinforces a shift towards proactive security. The ability to present positive test results can even be leveraged during negotiations to secure reduced rates or higher coverage limits. This means an organization's security spending transforms from a pure cost into a strategic investment. It allows organizations to shift from a reactive, "pay for the damage" mindset to a proactive, "invest to prevent" strategy. This isn't just about insurance; it's about overall financial resilience and risk management. Furthermore, the ability to negotiate better policy terms based on penetration test results means that organizations with a strong, validated security posture gain a competitive edge. It signals maturity and responsibility, which can also enhance customer trust and brand reputation, indirectly contributing to long term business value.

The formal penetration test report is the linchpin in demonstrating an organization's security posture to insurers. These reports are comprehensive documents detailing findings, providing concrete evidence, and offering actionable remediation guidance, making them crucial for both internal audits and developer action.

A well structured report should include an executive summary for high level stakeholders, a detailed scope and methodology, findings (including exploited vulnerabilities, their CVSS scores, business impact, and reproduction steps), concrete evidence, and clear, prioritized remediation recommendations. It's absolutely vital to maintain thorough documentation of all penetration test results, as this documentation serves as leverage when negotiating policy terms.

The formal, detailed penetration test report serves as the tangible, auditable artifact that translates technical security efforts into a language insurers understand: a validated risk posture and demonstrable due diligence. It's the "receipt" for proactive security investments. Insurers rely on quantifiable data to assess risk. A well structured penetration test report provides exactly that: it shows not just potential vulnerabilities but proven exploitable weaknesses, along with their business impact. This is far more compelling than a simple vulnerability scan report. It also outlines clear, actionable steps to fix issues, demonstrating a commitment to continuous improvement. Moreover, it serves as a formal record of security efforts, crucial for compliance and demonstrating "due care" if a breach does occur. This allows underwriters to move from a subjective assessment to a more objective, data driven evaluation of risk.

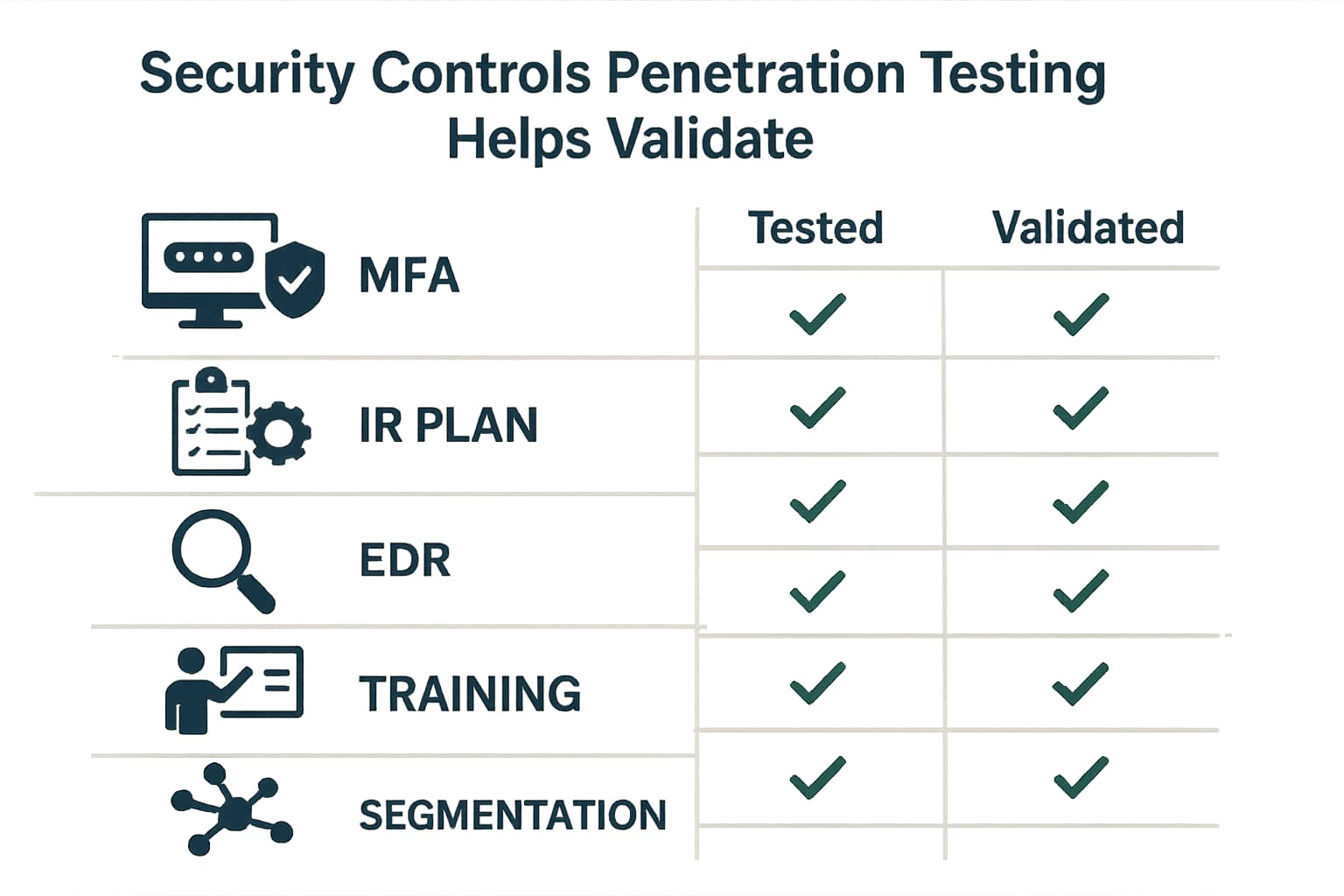

Cyber insurance providers are tightening their requirements in response to the escalating threat landscape. They want to see tangible evidence that organizations are actively managing their cyber risks. Penetration testing plays a direct role in validating many of these critical security controls.

Here’s a look at some key cybersecurity controls insurers typically look for, and how penetration testing provides the necessary validation:

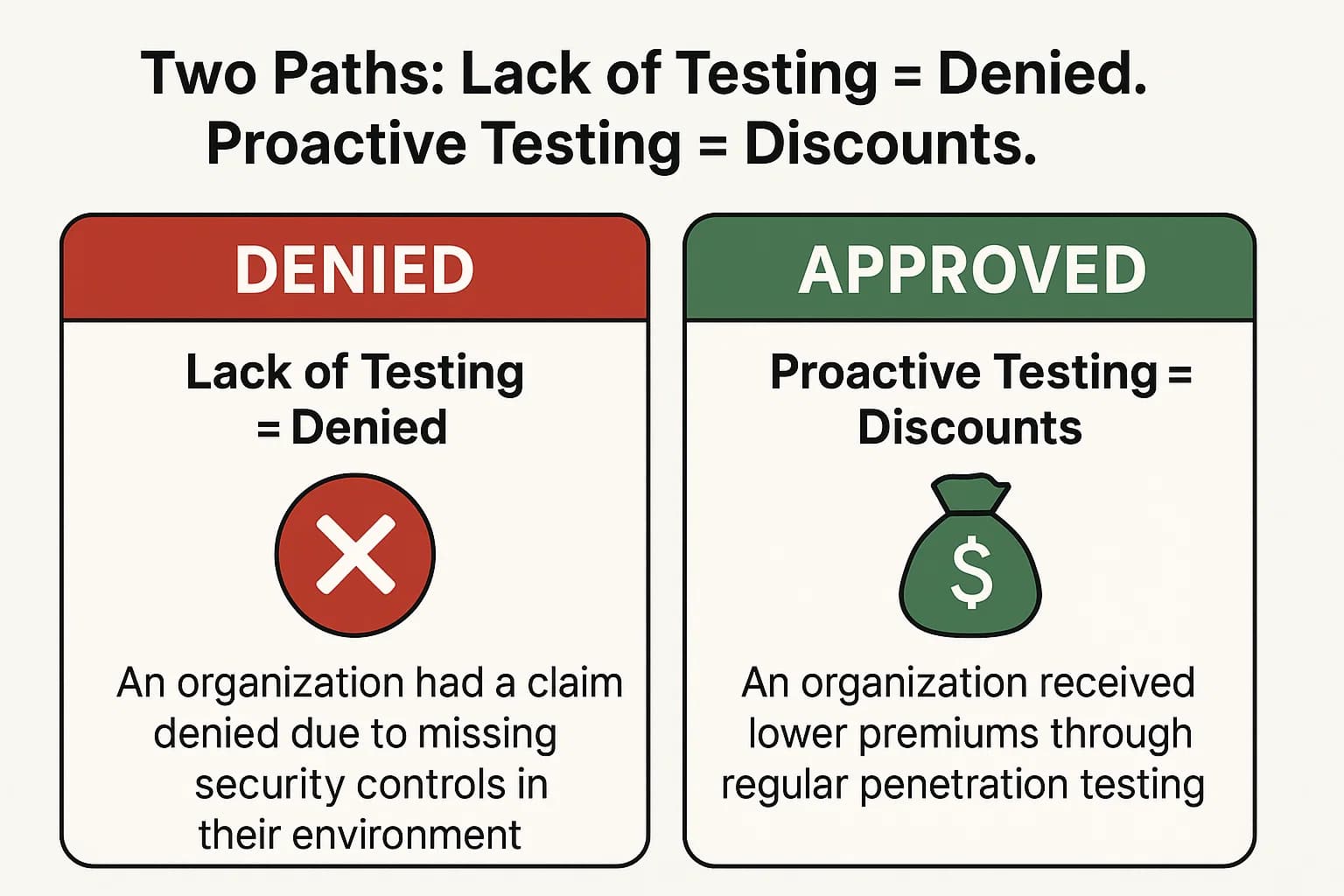

The value of penetration testing isn't just theoretical; it's proven in real world scenarios where its absence or presence can dramatically alter the outcome of a cyber incident.

Insurers are increasingly scrutinizing an organization's cybersecurity practices, and a lack of proper security testing can lead to denied claims or even the voiding of policies. The message is clear: organizations must demonstrate "due care".

These cases highlight a critical point: insurers frequently deny claims due to policy exclusions or a failure to implement necessary cybersecurity controls. The absence of comprehensive security testing, particularly penetration testing, leaves organizations vulnerable both to cyberattacks and to the financial repercussions of uncovered losses.

On the flip side, organizations that proactively invest in and document their penetration testing efforts often reap significant financial rewards from their cyber insurers.

The message is clear: investing in penetration testing isn't just a cost; it's an investment in risk reduction that pays dividends in both enhanced security and more affordable cyber insurance.

So, how does an organization practically weave penetration testing into its cyber insurance strategy? It comes down to a few key steps.

Cyber insurance is a specialized policy that protects organizations from the financial impacts of cyber incidents like data breaches, ransomware attacks, and network failures. It covers costs such as legal fees, digital forensics, data restoration, and breach notification. In 2025, with cybercrime projected to cost $10.5 trillion annually and average data breach costs reaching $4.88 million , it's essential because general liability policies typically exclude cyber risks, leaving businesses exposed to potentially catastrophic financial losses.

A vulnerability assessment (VA) uses automated tools to scan for and identify potential security weaknesses across a broad range of systems, telling you "what" and "where" vulnerabilities exist. vulnerability assessment vs penetration testing, on the other hand, is a manual, goal oriented simulation of a real attack by an ethical hacker who actively exploits vulnerabilities to determine "how" much damage an attacker could do and "so what" the real world business impact would be. Both are important, but PT provides the critical proof of exploitability.

While specific requirements vary by insurer and industry, most recommend at least annual penetration testing. For high risk industries (like finance or healthcare), or for organizations with frequent system changes or new deployments, quarterly or bi annual testing is often advised. Continuous penetration testing is also an option for agile environments to ensure ongoing security.

Yes, absolutely! Many insurance companies offer lower premiums to organizations that conduct regular penetration tests. By proactively identifying and remediating vulnerabilities, you reduce your overall risk profile, which insurers consider when setting policy costs. Positive test results and a demonstrated commitment to cybersecurity can also give you leverage to negotiate better terms and higher coverage limits.

If an organization fails to conduct required penetration testing or doesn't adequately address identified vulnerabilities, it risks having its cyber insurance claims denied. Insurers look for evidence of "due care" and adherence to stated security practices. A lack of proper security measures or documentation can lead to policy exclusions or even the voiding of coverage, leaving the organization to bear the full financial burden of a breach.

In the volatile landscape of 2025, where cybercrime costs are skyrocketing and breaches are a constant threat, cyber insurance is no longer optionality a fundamental component of business resilience. However, simply having a policy isn't enough. Insurers are demanding verifiable proof of robust cybersecurity practices, and that's where penetration testing shines.

Penetration testing provides an invaluable, real world assessment of an organization's defenses, moving beyond theoretical vulnerabilities to demonstrate actual exploitability and business impact. This proactive approach not only hardens systems against sophisticated attacks but also serves as undeniable evidence of "due care" to insurance providers. By identifying and remediating weaknesses before they can be exploited, organizations can significantly reduce their risk profile, leading to better cyber insurance eligibility, lower premiums, and more comprehensive coverage.

The strategic investment in regular, thorough penetration testing isn't just about compliance; it's about safeguarding financial stability, protecting reputation, and ensuring continuity in an increasingly dangerous digital world. It's the smart move for any organization looking to secure its future.

Need expert guidance? We’re here to help. Whether you’re planning a security strategy, facing compliance challenges, or just want an expert opinion drop us a line. At Deepstrike, we don’t sell fluff, just clear, actionable advice from real world practitioners.

Mohammed Khalil is a Cybersecurity Architect at DeepStrike, specializing in advanced penetration testing and offensive security operations. With certifications including CISSP, OSCP, and OSWE, he has led numerous red team engagements for Fortune 500 companies, focusing on cloud security, application vulnerabilities, and adversary emulation. His work involves dissecting complex attack chains and developing resilient defense strategies for clients in the finance, healthcare, and technology sectors.

Stay secure with DeepStrike penetration testing services. Reach out for a quote or customized technical proposal today

Contact Us